Retirement scenarios: How Fixed Term Investment can help your clients

Our scenarios are designed to help you understand the role Fixed Term Investment could play in your clients' retirement planning.

If you'd like to discuss specific examples, we'd love to talk to you.

These scenarios are for illustration purposes only.*

About Max, solution and outcome

Generate fixed monthly income until another secure income source begins - State Pension.

Max is aged 60 and he's semi-retired. He needs £11,500 per year until his State Pension starts in seven years. He wants to avoid drawing down on his portfolio in volatile markets.

Max invests £68,573.41 in an income-only Fixed Term Investment that has a seven-year term, delivering £958.33 monthly, paid gross into his pension cash account.

- Certainty of income for seven years regardless of market conditions.

- The solution works alongside his long-term investment strategy, minimising disruption.

- The income is paid with no tax deductions, allowing for tax-efficient withdrawals.

Need more information?

We've got a range of resources on Fixed Term Investment and the team is here to help you if you have specific questions.

About Isabella, solution and outcome

De-risking her portfolio to lock in value as she approaches retirement without exiting the market completely.

Isabella is aged 60, has £400,000 in her trust-based personal pension and plans to retire in five years. She’s concerned about market volatility impacting her personal pension in the run-up to retirement, but doesn’t want to exit existing investment strategies entirely.

Isabella allocates £150,000 into a five-year growth-based Fixed Term Investment. The plan has a guaranteed maturity amount of £191,437.48, while leaving the rest of her portfolio invested.

- Isabella has peace of mind knowing the exact amount she will receive on the plan’s maturity date.

- Part of her personal pension pot is protected from market swings, with the plan’s fund growth guaranteed.

- She has flexibility to stay invested with her remaining capital.

Need more information?

We've got a range of resources on Fixed Term Investment and the team is here to help you if you have specific questions.

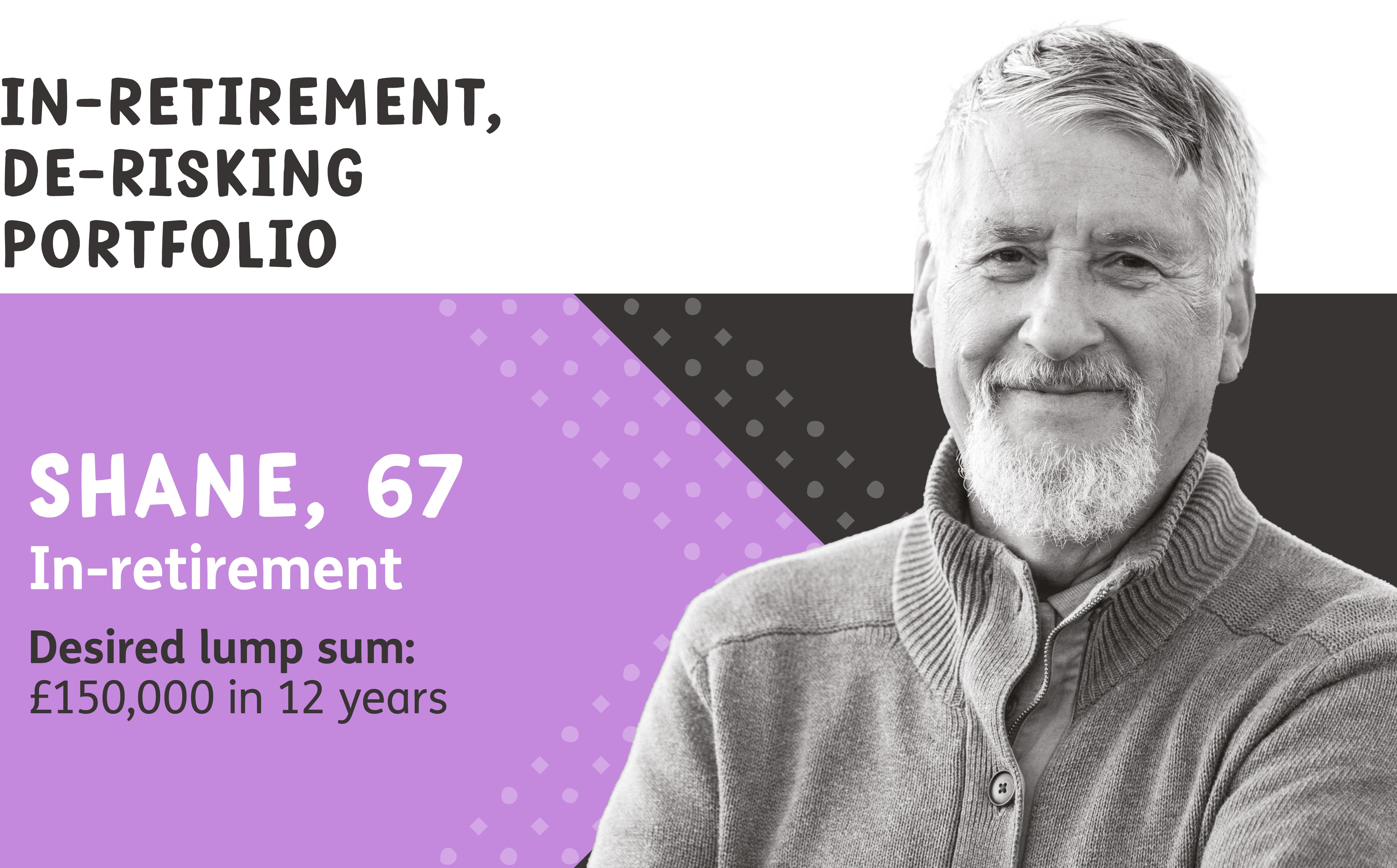

About Shane, solution and outcome

Secure capital for future potential care costs.

Shane is about to turn 68 and he’s already receiving his State Pension. He wants to use his personal pension to buy an investment that will guarantee he’ll have £150,000 available in 12 years (when he turns 80) to fund potential care costs. He doesn’t want to expose this money to market risk.

Shane uses £77,449.31 to purchase a 12-year growth-only Fixed Term Investment which guarantees a £150,000 lump sum at maturity.

- The lump sum is paid into Shane’s pension cash account with no tax deducted, allowing for tax-efficient withdrawals when the time comes.

- With the comfort of knowing there’ll be a fund available for his care when he anticipates he’ll need it, he can focus on his other priorities.

Need more information?

We've got a range of resources on Fixed Term Investment and the team is here to help you if you have specific questions.

Coming soon

*Notes:

1. Examples shown in the bridging income, pre-retirement de-risking growth and in-retirement de-risking growth scenarios are hypothetical and based on assumptions, not indicative of future performance. Provided for illustrative purposes only and should not be the sole basis for investment decisions. Investment returns can fluctuate. Scenario numbers are illustrative only, and correct as at 27 October 2025. If the client dies before the maturity date, Fixed Term Investment may pay a death benefit. Any income payments will stop and no maturity amount will be paid.

2. Please see the Technical guide for more information.